This month, inflation hit a new milestone. In February, annual inflation (as measured by the Consumer Price Index) jumped to 7.5%

You’ve probably felt the effects of inflation in your daily life. Trips to the grocery store are more expensive, filling your car is a budget buster, and maybe your rent has gone up on your latest lease.

But what does it mean that prices are 7.5 percent higher than the year before? How can we understand the effect of that number? We can start by using some basic economic and financial tools.

Inflation, Growth, and Levels

The first thing to note is that inflation is a rate not a level. A rate is something that happens over time. Why does that matter?

Imagine you spend $100 a week on groceries. Flash forward one year, and those same groceries cost you $107.50. Assuming the price increase happened throughout the economy, that means inflation was at a 7.5% annual rate according to the CPI measure.

Now imagine another year passes and the cost of those groceries remains at $107.50. If prices don’t rise then the annual rate of inflation has fallen to 0%. But notice, even with 0% inflation, in year two, the higher prices from year one don’t go away.

This is why it’s important to realize that inflation is a rate rather than a level. Unless there is some future deflation where prices fall, the prices will remain at a permanently higher level (from $100 to $107.50), even if no further inflation occurs.

Now it’s possible, even likely, that wages will rise to match these higher prices, but there’s no guarantee that this will happen before workers take a significant haircut in their real wealth relative to if there had been no inflation. Why?

Well first, because wages are unlikely to be the first prices to increase. So while your grocery bills are going up right away, your wage might not increase until your next annual review.

Second, as prices increase, the value of the money workers have in savings stays the same. So the rainy day fund you have tucked away for emergencies buys you less and less the longer inflation goes.

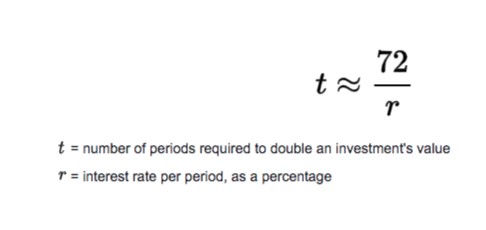

The Rule of 72

Now that we’ve seen how one-time inflation leads to permanently higher prices, what happens when inflation continues over time? What would it mean to maintain a 7.5 percent rate of inflation every year? After all, it’s hard to visualize what it means for something to grow 7.5 percent.

Our recent inflation report was an interesting milestone because of a “trick” used in finance to help think about how quickly things grow over time. That trick is called the “rule of 72”.

The rule of 72 is this–if you take a constant rate of growth of anything (savings accounts, price levels, or even the size of trees) and ignore the percent sign, then you divide 72 by that number, that will tell you how long it will be before the thing in question doubles in size.

Let’s consider the growth of prices. If prices grow at a rate of 7.5 percent annually we take 72 divided by 7.5 which comes to 9.6. What that means is, if annual inflation continues at a rate of 7.5%, the prices of goods in the economy in general will double in just less than 10 years. Basically, once you jump above a rate of 7.2 percent, you’re doubling prices every decade (or sooner when it’s higher).

Consider our example. If $100 grocery costs rise by 7.5 percent, that’s $107.50 at the end of one year. The next year that $107.50 also rises by 7.5 percent (107.50 x 1.075) to $115.56. If you do this multiplication ten times (one for each year) you have:

$100 x 1.075 x 1.075 x 1.075 x 1.075 x 1.075 x 1.075 x 1.075 x 1.075 x 1.075 x 1.075.

Or, simplified:

$100 x 1.07510

This brings our price of groceries at the end of 10 years to a little more than $208. As you can see, our prices have more than doubled.

So a 7.5% rate of inflation is a milestone of a sort, but the next question is, will this actually happen? Will 7.5% inflation persist every year for ten years? The answer is, at this point, it doesn’t seem likely.

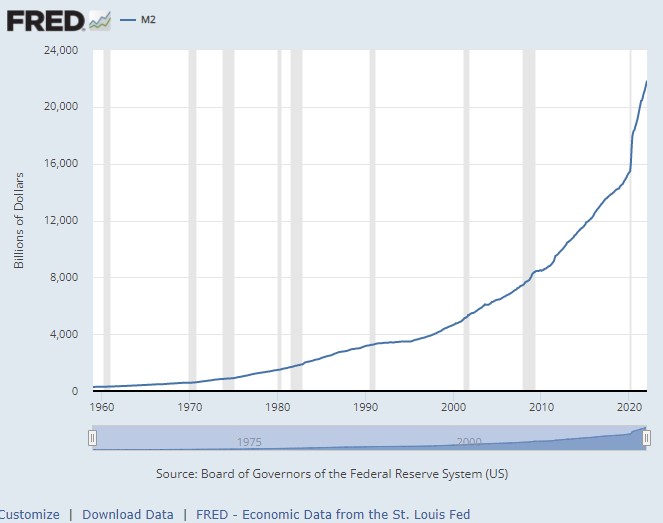

As I explained in a previous article, a significant factor in rising prices is the fact that the Federal Reserve has increased the supply of money (as measured by M2) nearly 42 percent since January of 2020. This graph from the St. Louis Federal Reserve shows this significant increase.

Ultimately, a 42 percent increase in the supply of money would eventually translate to prices increasing by, on average, the same amount according to the quantity theory of money (QTM) which was most famously developed by economist Milton Friedman.

If the QTM is correct, an increase in the money supply of 100% would be required for prices to double, everything else held constant.

So, as long as the Federal Reserve doesn’t go completely off the rails (which is by no means a given), prices likely won’t actually double in 10 years.

Yet, the rule of 72 still holds, and contains a dire warning.

The fact that, if inflation persisted at this same rate, it would take prices less than 10 years to double is reason for concern. We’re not under “hyperinflation,” but prices are certainly rising at a rate that troubles most Americans. And the rule of 72 helps us understand why their concern is warranted.

Author: Peter Jacobsen

Peter Jacobsen is an Assistant Professor of Economics at Ottawa University and the Gwartney Professor of Economic Education and Research at the Gwartney Institute. He received his PhD in economics from George Mason University, and obtained his BS from Southeast Missouri State University. His research interest is at the intersection of political economy, development economics, and population economics. He has previously written for both the Foundation for Economic Education and the Institute for Faith, Works, and Economics, and has been published in FEE, Reformed Perspective, National Review Online and Real Clear Markets, and co-hosts the Apple podcast “Faith and Economics.”

{kind=link}